Mark-0 COVID Heterogeneous-Agent ABM#

Mark-0 is a closed-economy ABM with \(N\) firms, one representative household, one commercial bank, and one central bank. The COVID extension [] adds the parameter set used to study V-, U-, L-, and W-shaped recovery regimes. Each macro period executes an ordered 24-phase loop: price/wage adjustment, hiring/firing, production, household consumption, interest-rate setting, bankruptcy, and firm revival.

Stochastic phases are reparameterised through three independent

frozen \(U(0, 1)\) noise buffers of shape (timesteps, N_firms)

pre-drawn in initialize(). Boundary conditions on the two

gradient-critical paths (stay_alive indicator and the positive-\(Y\)

guard) use Behavior.diffwhere; all other branches use plain

torch.where, matching the abmstat reference pattern.

Module Contents#

Mark0COVID is divided into Variables, Parameters (fixed constants), Scenarios, and the Behavior (model initialization and steps). See the sibling pages linked from the model index for the per-component tables.

Implementation in MacroStat#

The forward pass is differentiable end-to-end. The 24-phase loop is

decomposed into named methods on BehaviorMark0COVID so that each

phase carries its own docstring and Equations section.

ParametersMark0COVID.get_default_hyperparameters sets

dtype = torch.float64 to match the abmstat reference precision.

Model Dynamics#

Preparatory Steps#

%load_ext autoreload

%autoreload 2

import importlib

import logging

import sys

from matplotlib import pyplot as plt

from macrostat.models.Mark0COVID import Mark0COVID, ParametersMark0COVID

plt.style.use("../../macrostat.mplstyle")

importlib.reload(logging)

logging.basicConfig(stream=sys.stdout, level=logging.INFO)

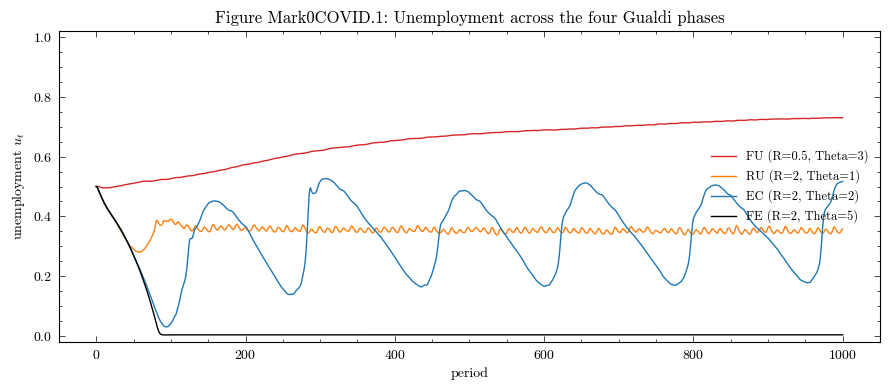

Four Gualdi phases#

show that the Mark-0 long-run regime is determined by the location of \((R, \Theta)\) in the parameter plane, where \(R = \eta_+/\eta_-\) is the hiring/firing asymmetry and \(\Theta\) is the bankruptcy default threshold. Four phases occupy distinct regions:

FU (Full Unemployment): \(R < R_c\), the economy collapses to near-zero employment regardless of \(\Theta\).

RU (Residual Unemployment): \(R > R_c\), low \(\Theta\); firms default quickly so a non-trivial unemployment rate persists.

EC (Endogenous Crises): \(R > R_c\), intermediate \(\Theta\); bankruptcy cascades trigger large oscillations between near-FE and near-FU regimes.

FE (Full Employment): \(R > R_c\), large \(\Theta\); defaults are rare and the economy sits near full employment.

Each phase is realised as a distinct ParametersMark0COVID

instance varying HiringFiringRate (\(R\)) and DefaultThreshold

(\(\Theta\)) only; all other parameters take their default values.

phases = {

"FU (R=0.5, Theta=3)": (0.5, 3.0),

"RU (R=2, Theta=0.5)": (2.0, 0.5),

"EC (R=2, Theta=1.2)": (2.0, 1.2),

"FE (R=2, Theta=5)": (2.0, 5.0),

}

paths = {}

for label, (R, Theta) in phases.items():

params = ParametersMark0COVID(

hyperparameters={"timesteps": 1000, "N_firms": 10000, "seed": 0},

)

params["HiringFiringRate"] = R

params["DefaultThreshold"] = Theta

model = Mark0COVID(parameters=params)

model.simulate()

paths[label] = model.variables.to_pandas()

Unemployment trajectory#

The aggregate unemployment series isolates the four phases at a glance. FU collapses to \(u \to 1\); RU settles at a positive residual; EC oscillates between near-FE and near-FU bands; FE converges close to full employment.

fig, ax = plt.subplots(figsize=(9, 4))

colors = ["tab:red", "tab:orange", "tab:blue", "k"]

for color, (label, df) in zip(colors, paths.items()):

ax.plot(df.index, df["Unemployment"], color=color, linewidth=1.0, label=label)

ax.set_title("Figure Mark0COVID.1: Unemployment across the four Gualdi phases")

ax.set_xlabel("period")

ax.set_ylabel(r"unemployment $u_t$")

ax.set_ylim(-0.02, 1.02)

ax.legend(loc="center right", frameon=False, fontsize=9)

plt.tight_layout()

plt.show()

Notes#

The shape of every het-agent state tensor in

model.variables.timeseriesis(T + 1, N_firms); aggregates are stored as(T + 1, 1).to_pandas()returns a multi-column DataFrame indexed bytime.