3IO-PCEX (IOPC)#

Model 30IO-PCEX was introduced by Marco Veronese Passarella as a simple pedagogical model and intermediate step towards an environmentally extended stock-flow consistent (SFC) input-output (IO) model (see the source repository). This implementation by Karl Naumann-Woleske extends the model to use the expectation version of model PC.

Module Contents#

As with all MacroStat models, IOPC is divided into Variables, Parameters (fixed constants), Scenarios, and the Behavior (model initialization and steps). The module-level documentation, such as all variables/parameters/scenarios and their notation or the behavioral equations associated with each function of BehaviorIOPC.py can be seen in:

For the full model API please check the API Reference

Model Overview#

The remainder of this page gives an introduction to the model, notes on how it is implemented in MacroStat and then shows some of the model dynamics using the default parameters.

Transaction Flow Matrix#

Household |

Government |

CentralBank |

CentralBank |

IOSectors |

Total |

|

|---|---|---|---|---|---|---|

Current |

Current |

Current |

Capital |

Current |

||

Nominal Consumption Household |

\(-p_c(t)c(t)\) |

\(+p_c(t)c(t)\) |

\(0\) |

|||

Nominal Consumption Government |

\(-p_g(t) g(t)\) |

\(+p_g(t) g(t)\) |

\(0\) |

|||

National Income |

\(+Y(t)\) |

\(-Y(t)\) |

\(0\) |

|||

Interest Earned On Bills Household |

\(+r(t-1)\cdot B_h(t-1)\) |

\(-r(t-1)\cdot B_h(t-1)\) |

\(0\) |

|||

Central Bank Profits |

\(+r(t-1)\cdot B_{CB}(t-1)\) |

\(-r(t-1)\cdot B_{CB}(t-1)\) |

\(0\) |

|||

Taxes |

\(-T(t)\) |

\(+T(t)\) |

\(0\) |

|||

Change in Money Stock |

\(+\Delta H_h(t)\) |

\(-\Delta H_{s}(t)\) |

\(0\) |

|||

Change in Bill Stock |

\(+\Delta B_h(t)\) |

\(-\Delta B_s(t)\) |

\(+\Delta B_{CB}(t)\) |

\(0\) |

||

Total |

\(0\) |

\(0\) |

\(0\) |

\(0\) |

\(0\) |

\(0\) |

Balance Sheet Matrix#

Household |

Government |

CentralBank |

IOSectors |

Total |

|

|---|---|---|---|---|---|

Current |

Current |

Capital |

Current |

||

Money Stock |

\(+H_h(t)\) |

\(-H_{s}(t)\) |

0 |

||

Bill Stock |

\(+B_h(t)\) |

\(-B_s(t)\) |

\(+B_{CB}(t)\) |

0 |

|

Wealth |

\(-V(t)\) |

\(+V(t)\) |

0 |

Model Dynamics#

Preparatory Steps#

%load_ext autoreload

%autoreload 2

import importlib

import logging

import sys

# Import the necessary libraries for plotting

from matplotlib import pyplot as plt

from matplotlib.ticker import PercentFormatter

# Import the MacroStat get_model function

from macrostat.models import get_model

from macrostat.causality import DocstringCausalityAnalyzer

# Custom matplotlib style for the documentation

plt.style.use("../../macrostat.mplstyle")

# We show the logging output in the notebook

importlib.reload(logging)

logging.basicConfig(stream=sys.stdout, level=logging.INFO)

The autoreload extension is already loaded. To reload it, use:

%reload_ext autoreload

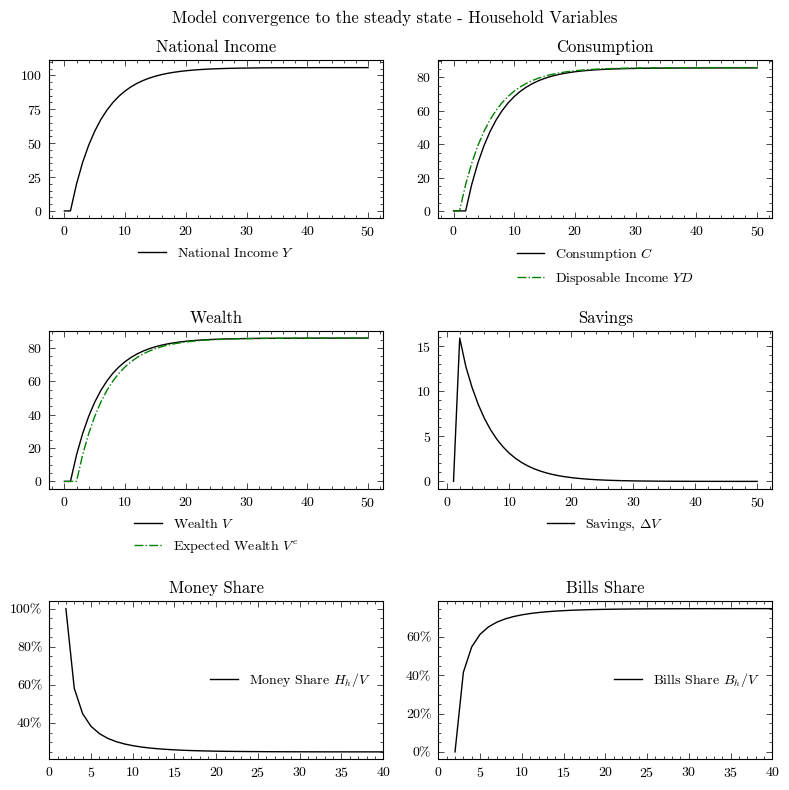

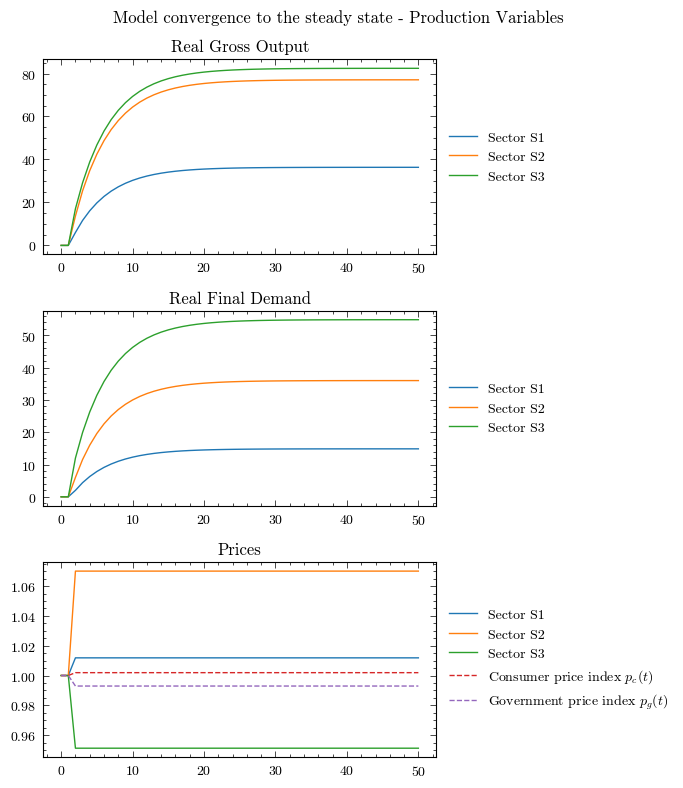

Running the Simulation#

First, we can run the model without any shocks to see the convergence to the steady state.

IOPCClass = get_model("IOPC")

model = IOPCClass()

model.simulate()

output = model.variables.to_pandas()

Here we can also check that the variables are healthy, which means that the redundant equations hold and that all the assets and liabilities are positive. For model PC, the redundant equation is that the household money stock equals the central bank money stock.

Note

In numerical implementations, due to floating point precision it is unlikely that the redundant equation will hold exactly. Therefore, we check that the absolute percentage error is less than a given tolerance, in this case 1e-5. We use the absolute percentage error to appropriately scale the error for different magnitudes of the variables.

model.variables.check_health(tolerance=1e-5)

True

Convergence to the Steady State#

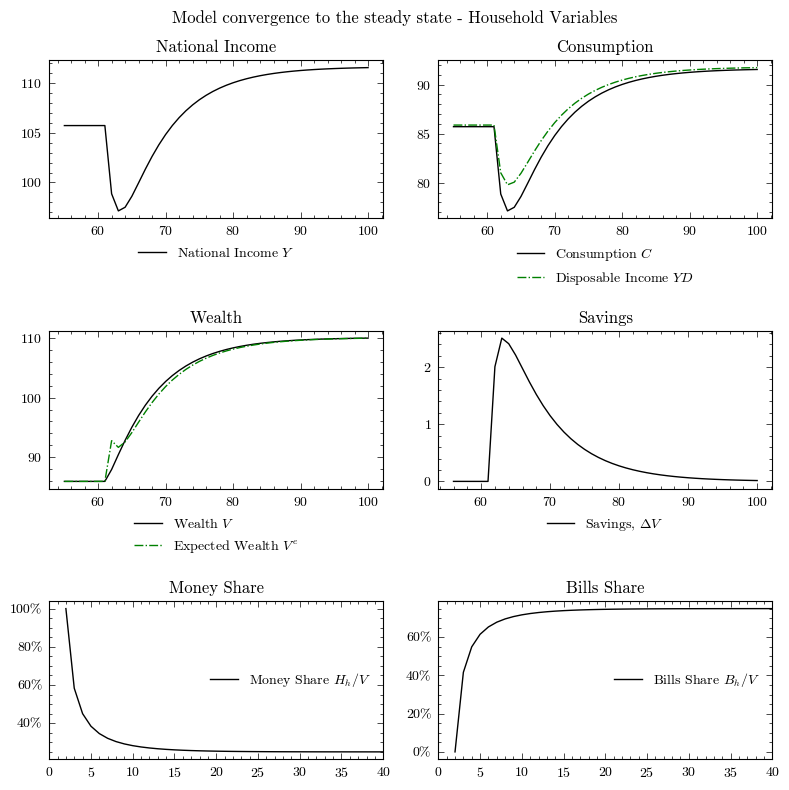

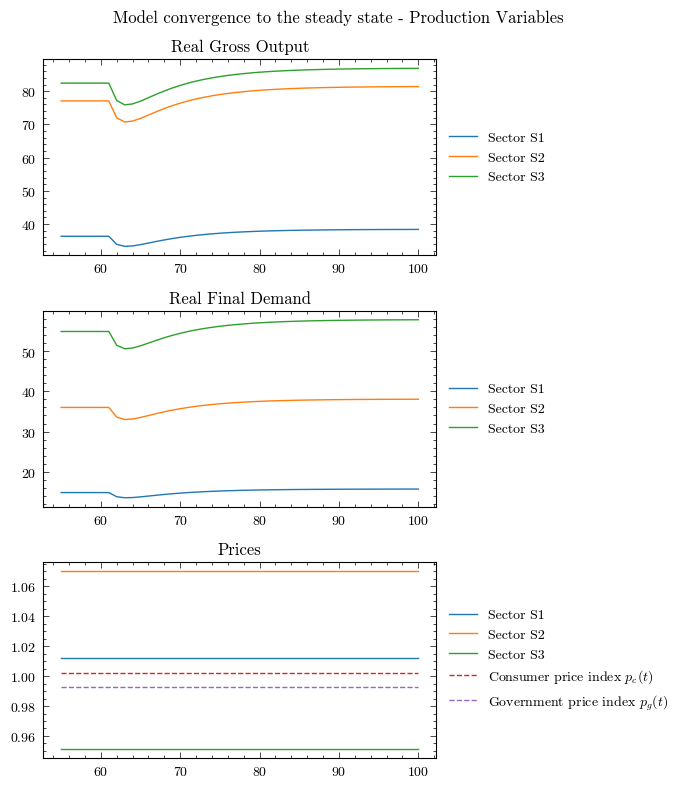

Perturbation 1: An increase of 100 points in the rate of interest on bills (\(r\))#

Following the convergence to the steady state, we can study the effects of an increase in the rate on bills by 100bps

MacroStat is set up to easily handle these scenarios. Much like in prior models, we simply define a new scenario IncreaseInterestRate and set the new rate to be 100 points higher \(r=0.025+0.01\)

model.parameters["scenario_trigger"] = 60

model.scenarios.add_scenario(

name="IncreaseInterestRate",

timeseries={"InterestRate":0.025 + 0.01}

)

model.simulate(scenario="IncreaseInterestRate")

output_rate_increase = model.variables.to_pandas()

Now we can see how the model reacts to the shock.

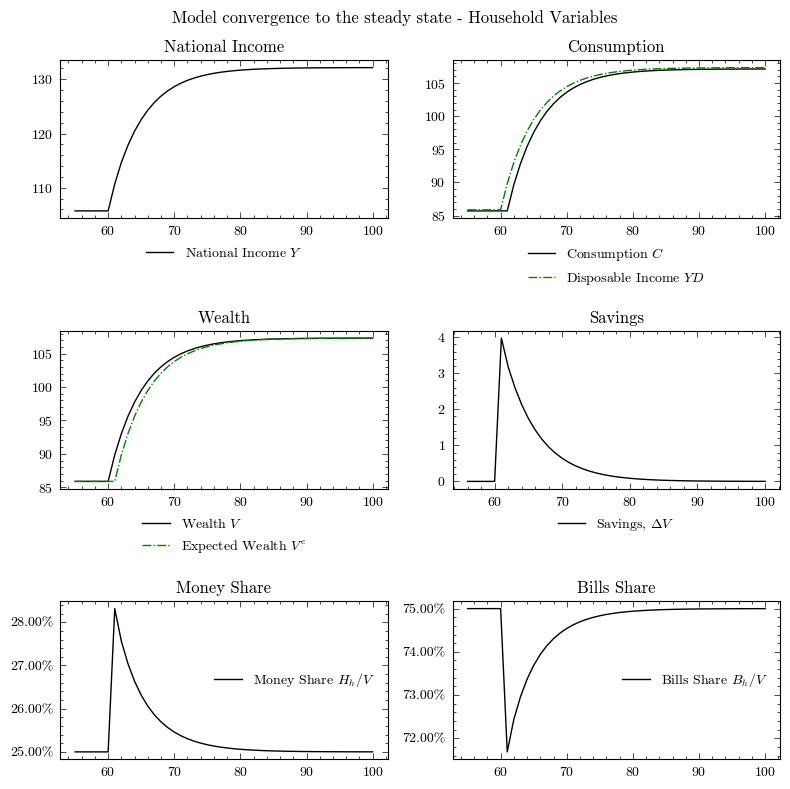

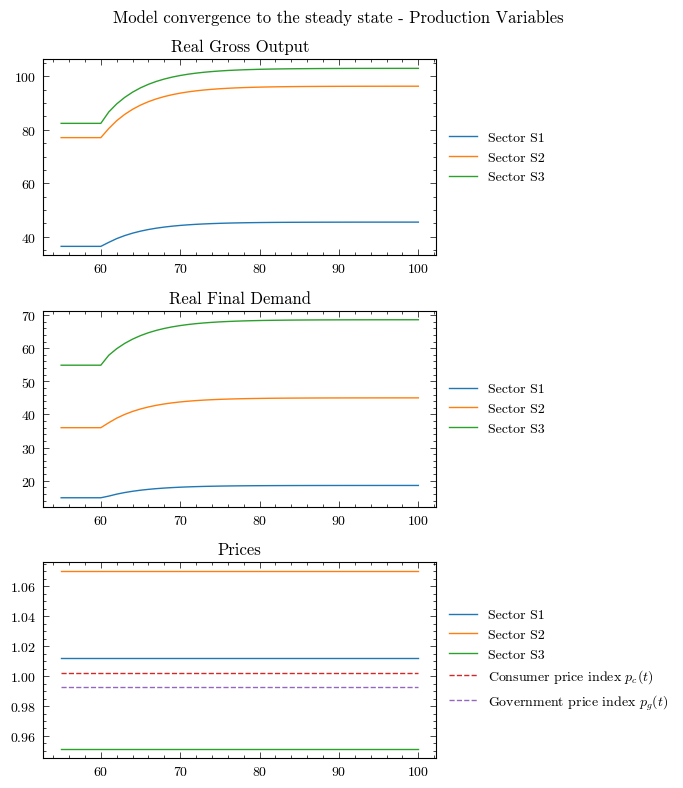

Perturbation 2: An increate in government spending#

model.parameters["scenario_trigger"] = 60

model.scenarios.add_scenario(

name="GovSpending",

timeseries={"GovernmentDemand":25}

)

model.simulate(scenario="GovSpending")

output= model.variables.to_pandas()

dfo = output.loc[55:]

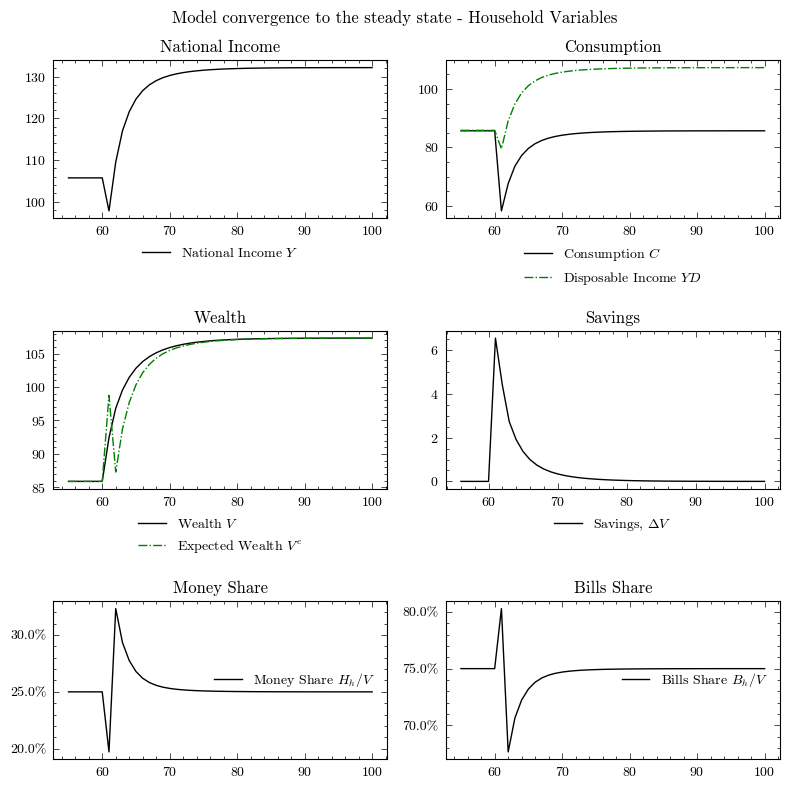

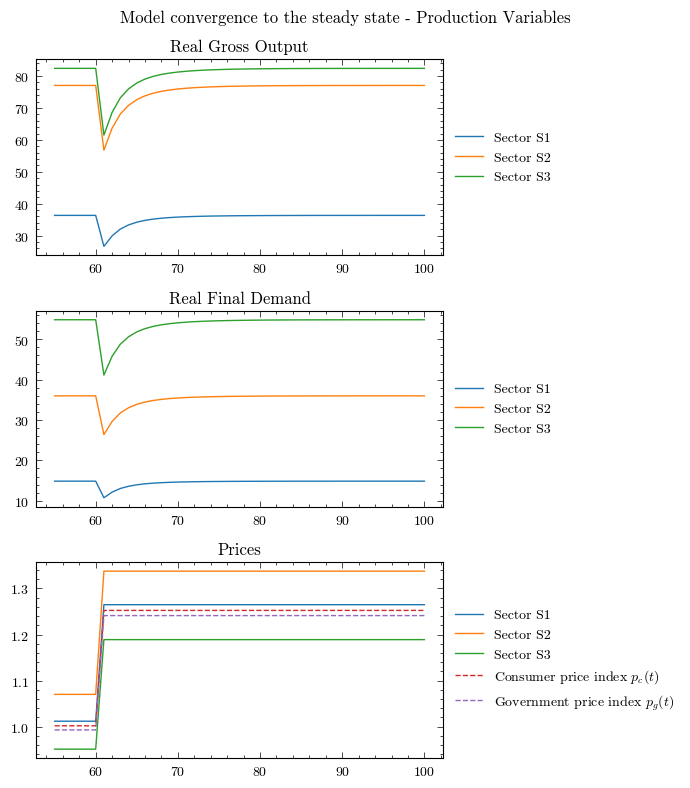

Perturbation 3: An increase in the wage rate#

model.parameters["scenario_trigger"] = 60

model.scenarios.add_scenario(

name="WageRate",

timeseries={"WageRate":0.5}

)

model.simulate(scenario="WageRate")

output_wage_rate_increase = model.variables.to_pandas()

dfo = output_wage_rate_increase.loc[55:]