Model LP#

Model LP is introduced in chapter 5 of Godley and Lavoie [2006] “Monetary Economics: An Integrated Approach to Credit, Money, Income, Production and Wealth”. It extends model PCEX by introducing long-term bonds, capital gains, and liquidity preference into the portfolio choice framework. Households now allocate their wealth across three assets: cash, Treasury bills, and long-term bonds.

Module Contents#

As with all MacroStat models, LP is divided into Variables, Parameters (fixed constants), Scenarios, and the Behavior (model initialization and steps). The module-level documentation can be seen in:

The remainder of this page gives an introduction to the model, notes on how it is implemented in MacroStat and then shows some of the model dynamics by replicating the relevant graphs of Godley and Lavoie (2006).

Model Overview#

Behavioral Equations#

Model LP extends model PCEX by adding long-term bonds to the household portfolio. The key innovations are:

Long-term bonds (\(BL\)) that pay a fixed coupon of 1 monetary unit per period

Bond prices (\(p_{bl}\)) that are set exogenously and can generate capital gains (\(CG\))

Three-asset portfolio choice across cash, bills, and bonds using Tobin’s framework

Expected returns on bonds that combine yield and expected capital gains

National Income

Disposable income now includes bond coupon income

Taxes now include bond income in the tax base

Wealth now includes capital gains from bond price changes

Capital gains arise from bond price changes

Consumption (unchanged from PCEX)

Expected wealth now includes capital gains

Bond yield is the inverse of the bond price

Expected return on bonds combines yield and expected capital gain

In the base LP model, the expected bond price equals the current bond price (static expectations)

Household demand for Treasury bills (Tobin portfolio allocation)

Household demand for bonds

Cash demand is the portfolio residual

Portfolio holdings equal demands

Realized household cash holdings

Government budget constraint now includes bond issuance

Central bank bill holdings and money supply

Expected disposable income (adaptive expectations)

With the redundant equation being

Note

In Model LP, the expected bond price \(p_{bl}^e = p_{bl}\) (static expectations), so the expected capital gain term in \(ERr_{bl}\) is always zero, and \(ERr_{bl} = r_{bl} = 1/p_{bl}\). Models LP2 and LP3 introduce adaptive expectations where \(p_{bl}^e \neq p_{bl}\).

Transaction Flow Matrix#

Household |

Production |

Government |

CentralBank |

CentralBank |

Total |

|

|---|---|---|---|---|---|---|

Current |

Current |

Current |

Current |

Capital |

||

Consumption Household |

\(-C(t)\) |

\(+C(t)\) |

\(0\) |

|||

Consumption Government |

\(+G(t)\) |

\(-G(t)\) |

\(0\) |

|||

National Income |

\(+Y(t)\) |

\(-Y(t)\) |

\(0\) |

|||

Taxes |

\(-T(t)\) |

\(+T(t)\) |

\(0\) |

|||

Interest On Bills Household |

\(+r_b(t-1) \cdot B_h(t-1)\) |

\(-r_b(t-1) \cdot B_h(t-1)\) |

\(0\) |

|||

Bond Coupon Income Household |

\(+BL_h(t-1)\) |

\(-BL_h(t-1)\) |

\(0\) |

|||

Central Bank Profits |

\(+r_b(t-1) \cdot B_{CB}(t-1)\) |

\(-r_b(t-1) \cdot B_{CB}(t-1)\) |

\(0\) |

|||

Change in Bill Stock |

\(+\Delta B_h(t)\) |

\(-\Delta B_s(t)\) |

\(+\Delta B_{CB}(t)\) |

\(0\) |

||

Change in Bond Stock |

\(+\Delta BL_h(t)\) |

\(0\) |

||||

Change in Bond Supply |

\(-\Delta BL_s(t)\) |

\(0\) |

||||

Change in Cash Stock |

\(+\Delta H_h(t)\) |

\(0\) |

||||

Change in Money Stock |

\(-\Delta H_s(t)\) |

\(0\) |

||||

Total |

\(0\) |

\(0\) |

\(0\) |

\(0\) |

\(0\) |

\(0\) |

Balance Sheet Matrix#

Household |

Production |

Government |

CentralBank |

Total |

|

|---|---|---|---|---|---|

Current |

Current |

Current |

Capital |

||

Wealth |

\(-V(t)\) |

\(+V(t)\) |

0 |

||

Bill Stock |

\(+B_h(t)\) |

\(-B_s(t)\) |

\(+B_{CB}(t)\) |

0 |

|

Bond Stock |

\(+BL_h(t)\) |

0 |

|||

Bond Supply |

\(-BL_s(t)\) |

0 |

|||

Cash Stock |

\(+H_h(t)\) |

0 |

|||

Money Stock |

\(-H_s(t)\) |

0 |

Implementation in MacroStat#

Transposing these equations to the MacroStat framework, we consider that there are:

Twelve parameters (fixed constants): \(\alpha_1\), \(\alpha_2\), \(\theta\), \(\chi\), and the eight \(\lambda\) portfolio coefficients (see Parameters)

Three scenario variables: \(G(t)\), \(r_b(t)\), and \(p_{bl}(t)\) (see Scenarios)

The remaining tracked series are variables (see Variables)

Model Dynamics#

Preparatory Steps#

%load_ext autoreload

%autoreload 2

import importlib

import logging

import sys

# Import the necessary libraries for plotting

from matplotlib import pyplot as plt

from matplotlib.ticker import PercentFormatter

# Import the MacroStat model components

from macrostat.models.GL06LP import GL06LP, ParametersGL06LP, ScenariosGL06LP

# Custom matplotlib style for the documentation

plt.style.use("../../macrostat.mplstyle")

# We show the logging output in the notebook

importlib.reload(logging)

logging.basicConfig(stream=sys.stdout, level=logging.INFO)

Running the Simulation#

First, we can run the model without any shocks to see the convergence to the steady state.

params = ParametersGL06LP()

model = GL06LP(parameters=params)

model.simulate()

output = model.variables.to_pandas()

We can check that the variables are healthy, meaning the redundant equation \(H_h = H_s\) holds and all stocks are positive.

Note

Due to floating point precision, the redundant equation will not hold exactly. We check that the absolute percentage error is below a tolerance.

model.variables.check_health(tolerance=1e-3)

True

An overview of the first 10 steps of the model:

df = model.variables.to_pandas()

df.head(10).T

| time | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ConsumptionHousehold | Household | 0.0 | 0.0 | 0.000000 | 16.124001 | 29.123171 | 40.013660 | 49.124569 | 56.747089 | 63.124352 | 68.459801 |

| ConsumptionGovernment | Government | 0.0 | 0.0 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 |

| NationalIncome | Macroeconomy | 0.0 | 0.0 | 20.000000 | 36.124001 | 49.123169 | 60.013660 | 69.124573 | 76.747086 | 83.124352 | 88.459801 |

| Taxes | Household | 0.0 | 0.0 | 3.876000 | 7.000832 | 9.618765 | 11.808908 | 13.641264 | 15.174274 | 16.456844 | 17.529890 |

| InterestOnBillsHousehold | Household | 0.0 | 0.0 | 0.000000 | 0.000000 | 0.191050 | 0.345075 | 0.474114 | 0.582067 | 0.672385 | 0.747948 |

| BondCouponIncomeHousehold | Household | 0.0 | 0.0 | 0.000000 | 0.000000 | 0.318207 | 0.574746 | 0.789669 | 0.969473 | 1.119904 | 1.245759 |

| CentralBankProfits | CentralBank | 0.0 | 0.0 | 0.000000 | 0.483720 | 0.491721 | 0.510488 | 0.525822 | 0.538661 | 0.549403 | 0.558390 |

| CapitalGains | Household | 0.0 | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| ExpectedCapitalGains | Household | 0.0 | 0.0 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 |

| Wealth | Household | 0.0 | 0.0 | 16.124001 | 29.123169 | 40.013657 | 49.124569 | 56.747089 | 63.124355 | 68.459801 | 72.923622 |

| HouseholdBillStock | Household | 0.0 | 0.0 | 0.000000 | 6.368336 | 11.502485 | 15.803792 | 19.402239 | 22.412830 | 24.931595 | 27.038883 |

| GovernmentBillStock | Government | 0.0 | 0.0 | 16.124001 | 22.759026 | 28.518745 | 33.331181 | 37.357616 | 40.726269 | 43.544609 | 45.902531 |

| CentralBankBillStock | CentralBank | 0.0 | 0.0 | 16.124001 | 16.390690 | 17.016260 | 17.527390 | 17.955378 | 18.313438 | 18.613014 | 18.863647 |

| HouseholdBondStock | Household | 0.0 | 0.0 | 0.000000 | 0.318207 | 0.574746 | 0.789669 | 0.969473 | 1.119904 | 1.245759 | 1.351054 |

| GovernmentBondSupply | Government | 0.0 | 0.0 | 0.000000 | 0.318207 | 0.574746 | 0.789669 | 0.969473 | 1.119904 | 1.245759 | 1.351054 |

| HouseholdCashStock | Household | 0.0 | 0.0 | 16.124001 | 16.390690 | 17.016258 | 17.527390 | 17.955381 | 18.313450 | 18.613026 | 18.863657 |

| CentralBankMoneyStock | CentralBank | 0.0 | 0.0 | 16.124001 | 16.390690 | 17.016262 | 17.527391 | 17.955379 | 18.313440 | 18.613014 | 18.863647 |

| DisposableIncome | Household | 0.0 | 0.0 | 16.124001 | 29.123169 | 40.013660 | 49.124569 | 56.747089 | 63.124352 | 68.459801 | 72.923615 |

| ExpectedDisposableIncome | Household | 0.0 | 0.0 | 0.000000 | 16.124001 | 29.123169 | 40.013660 | 49.124569 | 56.747089 | 63.124352 | 68.459801 |

| ExpectedWealth | Household | 0.0 | 0.0 | 0.000000 | 16.124001 | 29.123167 | 40.013653 | 49.124569 | 56.747089 | 63.124352 | 68.459801 |

| HouseholdBillDemand | Household | 0.0 | 0.0 | 0.000000 | 6.368336 | 11.502485 | 15.803792 | 19.402239 | 22.412830 | 24.931595 | 27.038883 |

| HouseholdBondDemand | Household | 0.0 | 0.0 | 0.000000 | 0.318207 | 0.574746 | 0.789669 | 0.969473 | 1.119904 | 1.245759 | 1.351054 |

| HouseholdCashDemand | Household | 0.0 | 0.0 | 0.000000 | 3.391522 | 6.125768 | 8.416473 | 10.332863 | 11.936184 | 13.277576 | 14.399836 |

| InterestRateBills | Macroeconomy | 0.0 | 0.0 | 0.030000 | 0.030000 | 0.030000 | 0.030000 | 0.030000 | 0.030000 | 0.030000 | 0.030000 |

| BondPrice | Macroeconomy | 0.0 | 0.0 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 |

| BondYield | Macroeconomy | 0.0 | 0.0 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 |

| ExpectedBondPrice | Household | 0.0 | 0.0 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 | 20.000000 |

| ExpectedReturnOnBonds | Household | 0.0 | 0.0 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 | 0.050000 |

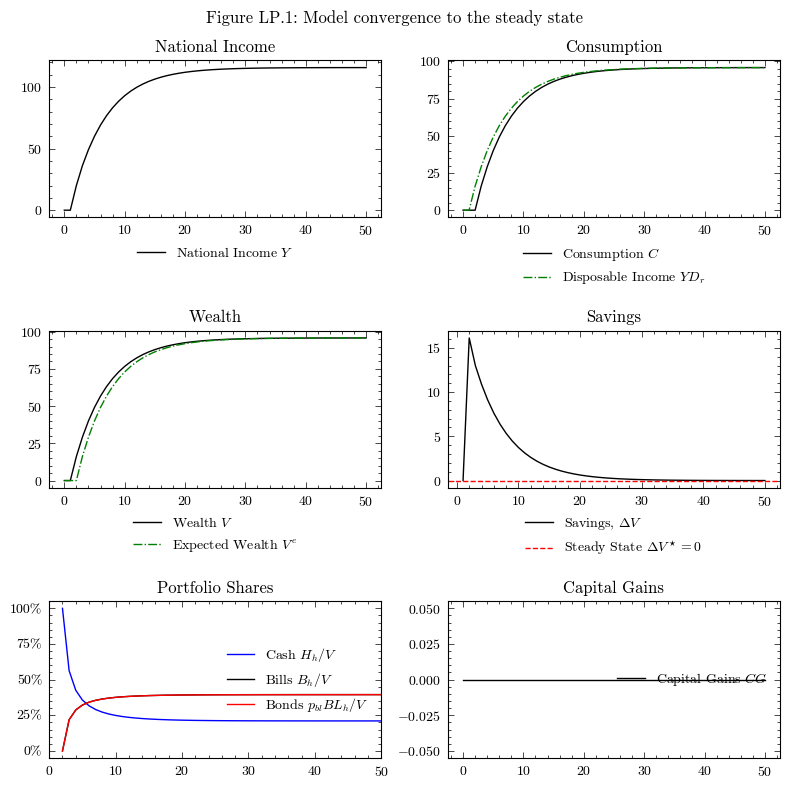

Convergence to the Steady State#

In the steady state of Model LP (with constant bond prices), capital gains are zero, and the model behaves similarly to PCEX but with three-asset portfolio choice. The household allocates its wealth across cash, Treasury bills, and bonds according to the Tobin portfolio equations.

Unlike earlier models, an analytical closed-form steady state is not straightforward for Model LP due to the additional portfolio equations and the interaction between bond yields and portfolio allocation. We therefore rely on the numerical convergence of the simulation.

dfo = output.loc[:50]

fig, axs = plt.subplots(ncols=2, nrows=3, figsize=(8, 8))

# National Income

axs[0, 0].plot(dfo.index, dfo['NationalIncome'], color='k', label=r'National Income $Y$')

axs[0, 0].legend(loc='upper center', bbox_to_anchor=(0.5, -0.1), frameon=False)

axs[0, 0].set_title('National Income')

# Consumption and Disposable Income

axs[0, 1].plot(dfo.index, dfo['ConsumptionHousehold'], color='k', label=r'Consumption $C$')

axs[0, 1].plot(dfo.index, dfo['DisposableIncome'], color='g', linestyle='-.', label=r'Disposable Income $YD_r$')

axs[0, 1].legend(loc='upper center', bbox_to_anchor=(0.5, -0.1), frameon=False)

axs[0, 1].set_title('Consumption')

# Wealth

axs[1, 0].plot(dfo.index, dfo['Wealth'], color='k', label=r'Wealth $V$')

axs[1, 0].plot(dfo.index, dfo['ExpectedWealth'], color='g', linestyle='-.', label=r'Expected Wealth $V^e$')

axs[1, 0].legend(loc='upper center', bbox_to_anchor=(0.5, -0.1), frameon=False)

axs[1, 0].set_title('Wealth')

# Savings

axs[1, 1].plot(dfo.index, dfo['Wealth'].diff(), color='k', label=r'Savings, $\Delta V$')

axs[1, 1].axhline(y=0, color='r', linestyle='--', label=r'Steady State $\Delta V^\star=0$')

axs[1, 1].legend(loc='upper center', bbox_to_anchor=(0.5, -0.1), frameon=False)

axs[1, 1].set_title('Savings')

# Portfolio Shares

cash_share = output['HouseholdCashStock'] / output['Wealth']

bill_share = output['HouseholdBillStock'] / output['Wealth']

bond_share = (output['HouseholdBondStock'].mul(output[('BondPrice','Macroeconomy')],axis=0)) / output['Wealth']

axs[2, 0].plot(output.index, cash_share, color='b', label='Cash $H_h/V$')

axs[2, 0].plot(output.index, bill_share, color='k', label='Bills $B_h/V$')

axs[2, 0].plot(output.index, bond_share, color='r', label='Bonds $p_{bl} BL_h/V$')

axs[2, 0].legend(loc='center right', frameon=False)

axs[2, 0].set_xlim(0, 50)

axs[2, 0].set_title('Portfolio Shares')

axs[2, 0].yaxis.set_major_formatter(PercentFormatter(1))

# Capital Gains

axs[2, 1].plot(dfo.index, dfo['CapitalGains'], color='k', label=r'Capital Gains $CG$')

axs[2, 1].set_title('Capital Gains')

axs[2, 1].legend(loc='center right', frameon=False)

fig.suptitle('Figure LP.1: Model convergence to the steady state')

plt.tight_layout()

plt.show()

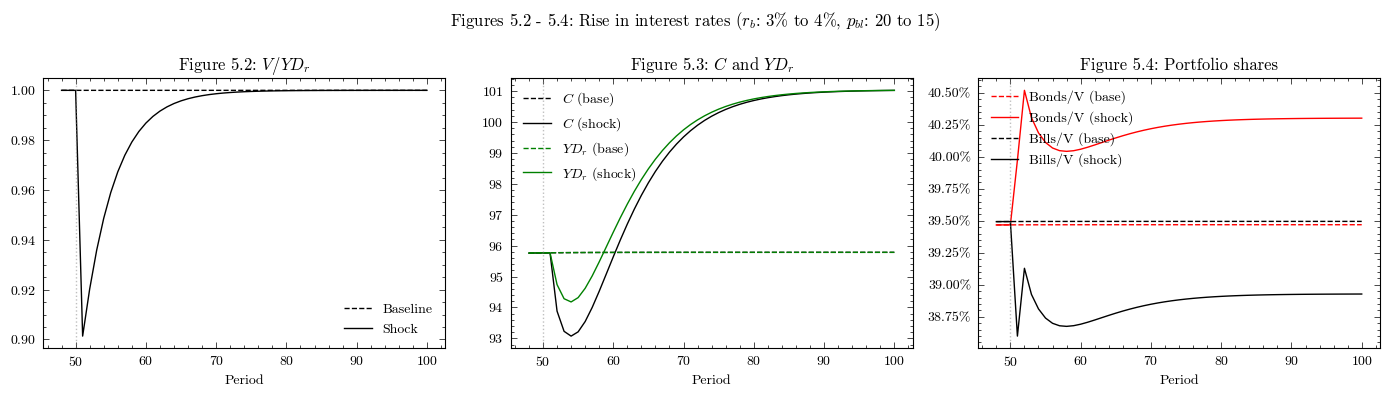

Perturbation 1: Increase in both short-term and long-term interest rates (Section 5.7)#

Following Section 5.7 of Godley and Lavoie [2006], we suppose there is an unexpected increase in the interest rates set by the monetary authorities. The bill rate rises from 3% to 4%, while the bond price drops from 20 to 15 (the bond yield rises from 5% to 6.67%). With static expectations (\(p_{bl}^e = p_{bl}\)), the expected return on bonds rises by the same amount as the yield.

The most important point of this experiment is that the fall in bond prices induces an immediate reduction in wealth through capital losses. This is one of the main conduits for monetary policy — a rise in interest rates reduces demand temporarily through the wealth channel in the consumption function. However, in the long run, the effect of higher interest rates is positive because higher debt service payments increase household income.

scenarios = ScenariosGL06LP(parameters=params)

sc1 = scenarios.get_scenario_index("Scenario.1: Rise in interest rates")

model1 = GL06LP(parameters=params, scenarios=scenarios)

model1.simulate(scenario=sc1)

output_sc1 = model1.variables.to_pandas()

trigger = params["scenario_trigger"]

dfo = output_sc1.loc[trigger - 2:]

dfo_base = output.loc[trigger - 2:]

fig, axes = plt.subplots(1, 3, figsize=(14, 4))

# Figure 5.2: V/YDr ratio

v_yd_base = dfo_base['Wealth'] / dfo_base['DisposableIncome']

v_yd_shock = dfo['Wealth'] / dfo['DisposableIncome']

axes[0].plot(dfo_base.index, v_yd_base, 'k--', label='Baseline')

axes[0].plot(dfo.index, v_yd_shock, 'k-', label='Shock')

axes[0].axvline(x=trigger, color='grey', linestyle=':', alpha=0.5)

axes[0].set_title('Figure 5.2: $V / YD_r$')

axes[0].set_xlabel('Period')

axes[0].legend(frameon=False)

# Figure 5.3: C and YDr

axes[1].plot(dfo_base.index, dfo_base['ConsumptionHousehold'], 'k--', label='$C$ (base)')

axes[1].plot(dfo.index, dfo['ConsumptionHousehold'], 'k-', label='$C$ (shock)')

axes[1].plot(dfo_base.index, dfo_base['DisposableIncome'], 'g--', label='$YD_r$ (base)')

axes[1].plot(dfo.index, dfo['DisposableIncome'], 'g-', label='$YD_r$ (shock)')

axes[1].axvline(x=trigger, color='grey', linestyle=':', alpha=0.5)

axes[1].set_title('Figure 5.3: $C$ and $YD_r$')

axes[1].set_xlabel('Period')

axes[1].legend(frameon=False)

# Figure 5.4: portfolio shares

bond_share_sc1 = output_sc1['HouseholdBondStock'].mul(output_sc1[('BondPrice',"Macroeconomy")],axis=0).div(output_sc1['Wealth'])

bill_share_sc1 = output_sc1['HouseholdBillStock'] / output_sc1['Wealth']

bond_share_base = output['HouseholdBondStock'].mul(output[('BondPrice',"Macroeconomy")],axis=0).div(output['Wealth'])

bill_share_base = output['HouseholdBillStock'] / output['Wealth']

axes[2].plot(bond_share_base.loc[trigger - 2:].index, bond_share_base.loc[trigger - 2:], 'r--', label='Bonds/V (base)')

axes[2].plot(bond_share_sc1.loc[trigger - 2:].index, bond_share_sc1.loc[trigger - 2:], 'r-', label='Bonds/V (shock)')

axes[2].plot(bill_share_base.loc[trigger - 2:].index, bill_share_base.loc[trigger - 2:], 'k--', label='Bills/V (base)')

axes[2].plot(bill_share_sc1.loc[trigger - 2:].index, bill_share_sc1.loc[trigger - 2:], 'k-', label='Bills/V (shock)')

axes[2].axvline(x=trigger, color='grey', linestyle=':', alpha=0.5)

axes[2].set_title('Figure 5.4: Portfolio shares')

axes[2].set_xlabel('Period')

axes[2].yaxis.set_major_formatter(PercentFormatter(1))

axes[2].legend(frameon=False)

fig.suptitle('Figures 5.2 - 5.4: Rise in interest rates ($r_b$: 3% to 4%, $p_{bl}$: 20 to 15)')

plt.tight_layout()

plt.show()

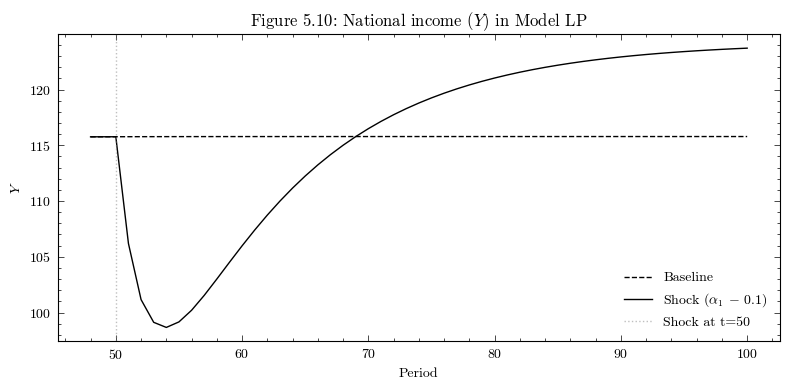

Perturbation 2: Sharp decrease in propensity to consume (Section 5.9, LP baseline)#

Following Section 5.9 of Godley and Lavoie [2006], we reduce the propensity to consume out of current income (\(\alpha_1\)) by 0.1. This has a negative short-run impact on GDP, but in Model LP (with exogenous government spending), the economy eventually recovers above the initial steady state. The larger saving leads to more government debt, higher interest payments, and hence higher disposable income in the long run.

This result serves as the crucial comparison with Model LP3 (Figure 5.10 vs Figure 5.11), where the fiscal austerity rule prevents the recovery.

scenarios = ScenariosGL06LP(parameters=params)

sc2 = scenarios.get_scenario_index("Scenario.2: Drop in alpha1")

model2 = GL06LP(parameters=params, scenarios=scenarios)

model2.simulate(scenario=sc2)

output_sc2 = model2.variables.to_pandas()

dfo = output_sc2.loc[trigger - 2:]

fig, ax = plt.subplots(figsize=(8, 4))

ax.plot(dfo_base.index, dfo_base['NationalIncome'], 'k--', label='Baseline')

ax.plot(dfo.index, dfo['NationalIncome'], 'k-', label='Shock ($\\alpha_1$ − 0.1)')

ax.axvline(x=trigger, color='grey', linestyle=':', alpha=0.5, label=f'Shock at t={trigger}')

ax.set_title('Figure 5.10: National income ($Y$) in Model LP')

ax.set_xlabel('Period')

ax.set_ylabel('$Y$')

ax.legend(frameon=False)

plt.tight_layout()

plt.show()